CLOSING THE RETIREMENT

GAP FOR A MORE SECURE

FUTURE

Many Singaporeans dream of a carefree retirement but inflation, rising healthcare costs and unexpected life events can get in the way. Early planning makes all the difference.

A comfortable retirement is the dream for many Singaporeans, yet for some, this may be less attainable today. Longer lifespans as well as rising healthcare and living expenses mean more savings are required to last through retirement. On top of that, some may aspire to retire early and work only when they choose to. Unexpected events such as caring for ageing parents or health setbacks also interrupt careers and limit the ability to save for retirement.

Despite these uncertainties, many still put off retirement planning. Financial services company Singlife found in its Financial Freedom Index 2024 that four in 10 Singapore consumers have yet to start preparing for retirement. Many say housing loans and saving for their children’s education come first. Some also assume that CPF Life – the national annuity plan – will be sufficient for their needs.

Planning ahead while you are younger helps build a more secure retirement.

Planning ahead while you are younger helps build a more secure retirement.

When retirement planning finally begins, many discover their savings are not enough. This shortfall – called the retirement gap – can be substantial. A DBS analysis of its retiree customers showed that the median CPF Life payout covers just over half of typical expenses, leaving the balance to be met through other income sources such as savings or investments.

WHY PLANNING EARLY MAKES THE DIFFERENCE

Financial planning experts say the first step to narrowing the retirement gap is to start early. Mr Stanz Tan, head of investments and wealth at Singlife, said the key is to determine your desired retirement lifestyle and assess what you have today. “Once you’ve done that, work with your financial adviser representative to map out a clear plan to close the gap,” he added.

That plan should take into account expected retirement expenses, which typically fall into three layers: essentials such as housing, food and transport; healthcare, including hospitalisation, medication and insurance premiums; and lifestyle expenses like holiday travel and entertainment. Each layer tends to increase over time and must be considered in any retirement plan.

Healthcare is often the most underestimated expense. “We have great healthcare in Singapore, but the costs associated with it can add up, especially for specialised treatment,” said Mr Tan. “While government schemes are helpful, they aren’t able to cover everything. In addition to these schemes, Singaporeans should consider having hospitalisation, critical illness and long-term care protection.” Studies suggest that long-term care can also add significant costs, averaging around S$3,000 a month. Mr Tan noted that keeping up with insurance coverage through retirement is essential to prevent gaps in protection when it is needed most. “We need to ensure we can sustain paying for these premiums in our retirement years,” he said. “Otherwise, a policy lapse could mean paying for healthcare out of pocket or even having to borrow from others.”

BUILDING AND PRESERVING WEALTH

Insurance is only part of the retirement equation. While it safeguards wealth, growing one’s savings is just as important. “Even after budgeting for essentials, healthcare and lifestyle, you may still face a retirement gap,” said Mr Tan. “To close it, you may need to reallocate part of your savings into investments. Higher returns come with higher risk, so diversification and professional advice are crucial.”

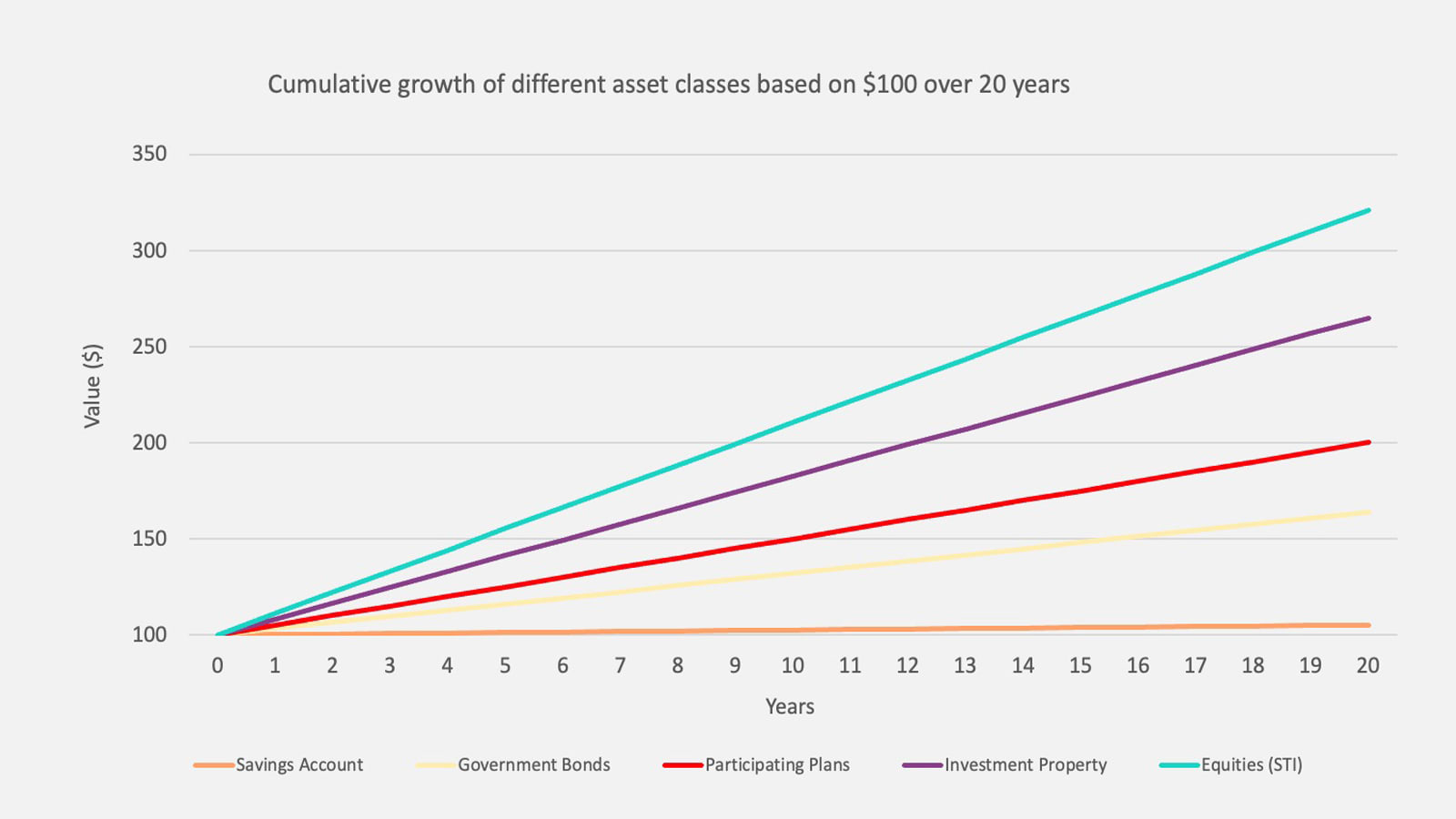

Diversification helps balance risk and return by spreading investments across different asset classes that perform differently over time. For instance, according to a chart prepared by Singlife (below), S$100 placed in a savings account would grow modestly to about S$105 after 20 years. Government bonds could reach S$164, while participating plans may offer a higher return of around S$200. Investment property could rise to about S$265, and equities show the strongest long-term growth potential at S$321. By selecting a mix of assets to invest in based on personal risk appetite, investors can benefit from this growth potential to reduce their retirement gap.

DIVERSIFICATION: BALANCING RISK AND RETURN

• CPF and cash savings alone may not fully close the retirement gap

• Other financial instruments can complement these savings to help manage longer-term needs

• Reviewing and diversifying investments across different asset classes can help balance risk and return

• Higher potential yields come with higher risk – seek professional advice before making investment decisions

Illustrative 20-year value growth of different asset classes, showing how diversification can help manage risk and return over time. (Chart: Prepared by Singlife)*

Illustrative 20-year value growth of different asset classes, showing how diversification can help manage risk and return over time. (Chart: Prepared by Singlife)*

To support both protection and growth, insurance savings or investment-linked plans are options. Singlife’s Singlife Flexi Retirement II plan provides guaranteed, customisable payouts, while Singlife Legacy Invest is an investment-linked plan designed to help customers achieve better returns.

Singlife also offers two investment platforms under its subsidiary for different investor preferences. DollarDex, a no-fee platform backed by Singlife, gives self-directed investors access to a broad range of solutions, including options that allow the use of CPF and Supplementary Retirement Scheme savings. Many people need guided support from a trained adviser. For these consumers, Grow with Singlife works with nearly 5,000 financial adviser representatives across 46 advisory firms and partners leading asset managers – including BlackRock, Fullerton Fund Management, Aberdeen and Lion Global Investors – to offer exclusive tailored investment options.

Both platforms support diversification by providing access to global equity, fixed-income and multi-asset funds, including income- and growth-oriented products. Mr Farooq Lone, CEO of Grow with Singlife, said that DollarDex is “good for those who are disciplined, savvy and want to manage their own investments”. “However, most consumers will benefit from the support of a wealth planning expert,” he added. “Grow with Singlife works to equip financial adviser representatives to deliver deeply personalised service and guidance to help their clients achieve financial freedom.”

Mr Lone added that the goal is to help investors stay prepared as they plan for longer retirements. “As lifespans extend and Singaporeans spend more years in retirement, many of us risk falling short of the income we’ll need in our sunset years,” he said. “Insurance is critical, but more can be done to bridge the retirement gap.”

(Photo: Mediacorp Studio 3)

(Photo: Mediacorp Studio 3)

“BY PAIRING INSURANCE THAT SAFEGUARDS AGAINST LONG-TERM HEALTHCARE WITH DISCIPLINED INVESTING TO GROW WEALTH OVER TIME, YOU CAN PAVE A BETTER WAY TO CLOSING THE GAP AND SUSTAINING YOUR DESIRED LIFESTYLE IN RETIREMENT.”

– MR FAROOQ LONE, CEO OF GROW WITH SINGLIFE

Planning for retirement does not end once savings and investments are in place. It also involves managing how those funds are drawn down so they last through the retirement years. Without a clear strategy, retirees risk spending too quickly or being overly cautious and compromising their quality of life. “Decumulation means assessing what you have and how to use it to fund your retirement years,” said Mr Tan. This can mean setting up staggered payouts from annuities or income plans, or downsizing a home once the children have moved out.

As needs change, regular reviews of insurance and overall protection are essential. Those who have paid off major liabilities or whose children are financially independent should reassess both their insurance and broader retirement plans to ensure they match current needs. Despite the challenges, reaching retirement goals is possible with discipline, planning and timely action.

(Photo: Mediacorp Studio 3)

(Photo: Mediacorp Studio 3)

“THE KEY IS TO START WITH A PLAN THAT FITS YOUR SITUATION AND OPTIMISING THE SAVING HORIZON YOU HAVE. EVEN THOSE IN THEIR 40s OR 50s CAN MAKE PROGRESS WITH THE RIGHT MIX OF PROTECTION, INVESTMENT AND INCOME STRATEGIES.”

– MR STANZ TAN, HEAD OF INVESTMENTS AND WEALTH AT SINGLIFE

Ultimately, the retirement journey is about confidence – knowing you have a clear plan to sustain your lifestyle, manage healthcare costs and stay financially independent. The earlier that path begins, the better equipped you will be to close the retirement gap.

*Prepared by Singlife using information from:

https://tradingeconomics.com/singapore/deposit-interest-rate

https://www.investing.com/rates-bonds/singapore-20-year-bond-yield-historical-data

https://www.forecast-chart.com/historical-straits-times.html

https://www.globalpropertyguide.com/asia/singapore

/price-history

https://www.milliman.com/en/insight/singapore-2025-participating-fund-health-check

Disclaimer:

This article is published for general information only and does not have regard to the specific investment objectives, financial situation and particular needs of any specific person. This advertisement has not been reviewed by the Monetary Authority of Singapore. DollarDex and Grow with Singlife are operated by Navigator Investment Services Ltd, a subsidiary of Singapore Life Ltd (Singlife). Protected up to specified limits by SDIC.

Information is correct as at December 5, 2025.